Page 18 - Securities_Lending_Market_Report_-_June_2022

P. 18

18 19

Securities Lending Market Report | June 2022

>>> North America Equity

Fig 6 - S&P Global The US IPO market slumped sharply in the 2nd quarter with a decline of 73% for the number of deals and a

95% drop in proceeds YoY. The SPAC market continued to collapse with just 15 blank check IPOs and 19 merger

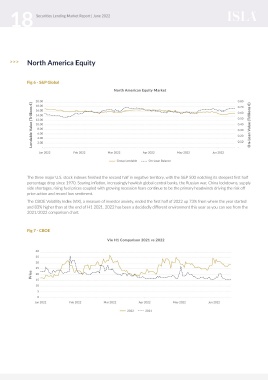

North American Equity Market

completions. While several large IPOs in the pipeline updated their filings during the quarter, new filings sank to a

six year low.

20.00 0.80

Lendable Value (Trillions €) 14.00 0.50 On-Loan Value (Trillions €) Fig 8 - Stock Analysis H1 IPO Comparison 21/22

18.00

0.70

16.00

0.60

12.00

0.40

10.00

8.00

160

0.30

6.00

0.20

4.00

140

2.00

-

-

Number of US IPO’s 80

Jan 2022 Feb 2022 Mar 2022 Apr 2022 May 2022 Jun 2022 0.10 120

100

Group Lendable On-Loan Balance

The three major U.S. stock indexes finished the second half in negative territory, with the S&P 500 notching its steepest first half 60

percentage drop since 1970. Soaring inflation, increasingly hawkish global central banks, the Russian war, China lockdowns, supply 40

side shortages, rising fuel prices coupled with growing recession fears continue to be the primary headwinds driving the risk off

price action and record low sentiment. 20

The CBOE Volatility Index (VIX), a measure of investor anxiety, ended the first half of 2022 up 73% from where the year started 0

and 83% higher than at the end of H1 2021. 2022 has been a decidedly different environment this year as you can see from the Jan Feb Mar Apr May Jun

2021/2022 comparison chart. 2022 2021

Fig 7 - CBOE

M&A deals were also significantly down compared to Finally, on the ETF front, bond volatility and the ongoing

Vix H1 Comparison 2021 vs 2022 2021 which was the most active year on record. Newly inflation concerns resulted in continued demand for high

announced deals in 2022 are down 31% versus 2021 and yield bond ETFs including IShares IBoxx High Yield Bond

40 the slowdown is expected to continue. ETF (HYG) and SPDR Bloomberg Barclays High yield Bond

35 The top five sectors that were in demand in the first half ETF (JNK) as well as the IShares Trust IBoxx Investment

30 of the year were Consumer Discretionary, Industrials, Grade Corporate Bond ETF (LQD) as dealers borrowed

25 Information Technology, Financials, and Health Care. as a hedge against widespread credit issues and bond

Price 20 The Electric Vehicle space, which are heavily represented defaults. There were large outflows throughout the 2nd

15 in the Consumer Discretionary and Industrials, once quarter as investors were on edge with the expected

10 again performed strongly from a lending perspective in interest rate hikes, creating wider spreads due to reduced

5 the second quarter of 2022 with the demand driven by lendable supply industry wide.

0 continued chip shortages and supply chain issues which

Jan 2022 Feb 2022 Mar 2022 Apr 2022 May 2022 Jun 2022 have severely hampered production.

2022 2021