Page 18 - 2516_21_June_ISLA_Market_Report_-_March_2022_final

P. 18

18 19

Securities Lending Market Report | March 2022

>>> US >>> Final Thoughts & Looking Ahead

As securities lending increased globally by almost 35%, driven by new IPOs, asset price inflation, introduction of

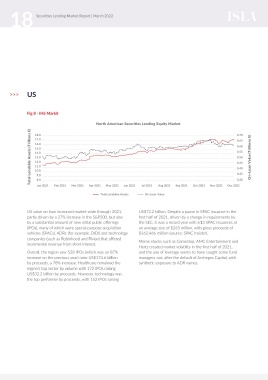

Fig 8 - IHS Markit

liquidity outside usual agent lenders (Canadian banks, CP issuance vehicles, hedge funds), and new beneficial owners

entering/re-entering the market, the securities lending product became increasingly commoditised. Lenders looked to

North American Securities Lending Equity Market

collateral schedules and technology as a way to differentiate themselves, and expansion of acceptability within collateral

Total Lendable Assets (Trillions €) 16.0 0.60 On-Loan Value (Trillions €) Technology continues to create considerable interest. New markets will always be of interest to lenders and

schedules continued through the year –China Connect being a good example. This expansion of acceptability goes hand

0.70

18.0

in hand with a growing risk appetite, as markets steadied following the volatility peaks in 2020.

17.0

0.65

15.0

borrowers alike, and the modernisation trend through

After three to four years of offerings on lending platforms,

0.55

14.0

some clear winners are emerging, with more volumes

the Middle East offers substantial opportunity. HSBC is

0.50

13.0

traded via straight through processing (STP) than ever

proud to have completed the first ever lending transaction

12.0

0.45

before, and many securities financing providers offering

in Saudi Arabia and we look forward to more such

11.0

0.40

10.0

opportunities in ‘frontier’ markets in the imminent horizon.

third-party technology solutions as a way to differentiate

0.35

9.0

themselves. Around 95% of the trades HSBC executes in

8.0

0.30

agency lending, on behalf of our clients, are automated and

several regulations that were delayed due to COVID-19 are

May 2021

Jun 2021

Feb 2021

Mar 2021

Apr 2021

Jan 2021

Oct 2021

Nov 2021

Dec 2021

Jul 2021

Aug 2021

Sep 2021

fully STP. Clients can gain from the data-driven analytical The regulatory agenda continues to consume resource and

now coming through. After a number of delays, the Central

Total Lendable Assets On-Loan Value functions that are available, with the aim of enhancing Securities Depositories Regulation (CSDR) Settlement

customer value and client returns.

Discipline Regime (SDR) went live in February 2022. The

We have also seen an emerging focus on digitising/digital heavily discussed mandatory buy-in rules for failed trades

US value on loan increased market-wide through 2021, US$72.2 billion. Despite a pause in SPAC issuance in the ledger technology; and the prospect of a new digital asset have been delayed, but firms still need to comply with the

partly driven by a 27% increase in the S&P500, but also first half of 2021, driven by a change in requirements by class that uses tokenisation is looming, bringing with it other elements of the SDR, including enhanced reporting

by a substantial amount of new initial public offerings the SEC, it was a record year with 613 SPAC issuances at both risk and opportunity. Momentum behind tech-driven and cash penalties in the event of a failed trade settlement.

(IPOs), many of which were special purpose acquisition an average size of $265 million, with gross proceeds of strategies has been accelerated by homeworking trends

vehicles (SPACs), ADRs (for example, DIDI) and technology $162,466 million (source: SPAC Insider). during lockdowns, which have fuelled the need to increase Increased regulation can bring positives too. Securities

companies (such as Robinhood and Rivian) that offered Meme stocks such as Gamestop, AMC Entertainment and existing trading automation. Financing Transactions Regulation (SFTR) and data sharing

incremental revenue from short interest. have led to more transparency in the marketplace, which

Hertz created market volatility in the first half of 2021, As securities financing participants focus on the bottom has added to a feeling of confidence. We hope this

Overall, the region saw 528 IPOs (which was an 87% and the use of leverage seems to have caught some fund line, technology is not the only way to drive efficiency. transparency will expand into the US and other markets,

increase on the previous year) raise US$174.6 billion managers out, after the default of Archegos Capital, with Integration of businesses through the securities financing helping to address any negative concerns associated to the

by proceeds, a 78% increase. Healthcare remained the synthetic exposure to ADR names. chain, from a full resource and infrastructure perspective, lending business.

region‘s top sector by volume with 172 IPOs raising is a trend that we are seeing more prominently across the

US$32.2 billion by proceeds. However, technology was marketplace. At HSBC, for example, we have combined our It is shaping up to be a very different year in 2022. The

the top performer by proceeds, with 152 IPOs raising Securities Services and Markets businesses and are soon global economic recovery has meant attention was focused

launching US Arranged Financing to connect US asset on central banks, policymakers, and the short term for much

of 2021. The alarm around the pandemic seems to have

managers with Eastern markets.

abated to an extent, and the focus can now be directed

Aligning with ESG principles and using cutting-edge on the longer term. The industry is now rebalancing itself

technology/automation is also likely to give market where governments, markets, companies, and investors all

participants an edge. Different regions, funds and look to navigate the post COVID environment. This should

investment strategies require different ESG lenses, so lead to increased securities lending demand, creating

having a banking partner with the ability to support ESG opportunities ahead for investors with the right strategy

along with a global reach can be hugely beneficial. and the right partnership to help them grow and prosper.