Page 10 - 2808_24_Jan_ISLA_Market_Report_-_Feb_2024_-_final

P. 10

10 11

Securities Lending Market Report | December 2023

EMEA

>>> As mentioned in our introductory comments, the second half of the year in the EMEA region has fared little to no better Fig 2 - DataLend

that the previous two quarters – in fact, if anything, in securities lending terms it has worsened. We have continued to

see interest rates raise across the region in what has now looked to be a successful manoeuvre in containing inflation. European Equity Market Cash vs Non-Cash

Numbers suggest that towards the end of Q3 and into Q4 inflation was at a steady decline in the more developed

economic countries. Unfortunately, we have seen an upsurge in activity in the Ukraine and Russia Conflict which 30.00 180.00

continues to put pressure on many industries including shipping and energy forcing financial institutions to navigate 25.00 150.00

around the situation at potentially great cost which is absorbed into the transactions in which many of us are engaged.

In October Palestine militants launched an attack at Gaza. The conflict is ongoing and is yet another major geo-political 20.00 120.00

event effecting global markets and creating volatility. As with the Ukraine situation, shipping costs are in focus with most On-Loan vs Cash (Billions €) 15.00 90.00 On-Loan vs Non-Cash (Billions €)

shipping companies avoiding the Red Sea and Suez Canal route.

Looking at the specials market in EMEA, it has been very Balances took the usual seasonal tumble during the summer 10.00 60.00

crowded with little to no new activity, interest remains in period, and it has been a very slow burn into the final 5.00 30.00

a handful of directional names that have pressure on the quarter. A name of note in the UK market is Manchester- 0.00 0.00

share price and increasing lending fees which ultimately based Boohoo Group plc, we saw significant utilization Jul 23 Aug 23 Sep 23 Oct 23 Nov 23 Dec 23

results in flat alpha. Small and mid-cap names have led the and fee increases in this name on the back of a $197mm

charge when it comes to event driven or special situation settlement in the US for fake discount advertising, just Group Balance vs Cash Group Balance vs Non Cash

opportunities across a number of countries but margins another incident for the troubled company which remains on

have been thin. Revenues in European equities dropped every lenders’ watch list as more and more clients take short

significantly, by 25%, in Q3 year on year, and whilst fared positions in the name. Fig 3 - DataLend

a little bit better in Q4 were still down a further 10%. Fees Also in the UK, it was good to see the continuation of the

declined by more than 40% in the UK and Sweden in Q4 UK scrip dividend for SSE. This provides revenue for all European Government Bond Market Cash vs Non-Cash

and there were very few bright spots to talk about.

lenders and was a rare positive for London based traders as

With the cost of Capital at an all-time high we have seen borrowers look to benefit from differences between cash 25.00 350.00

the large blue-chip companies sit somewhat in the shadows and stock options. 20.00 300.00

with little to no activity. The number of third-quarter deal Fixed Income has seen balances remain fairly level in

announcements fell 36.4% year over year to the lowest level comparison to equities with lots of demand in the credit/ 15.00 250.00

since the second quarter of 2020. rates and High Yield space. Again, the high-rate environment On-Loan vs Cash (Billions €) On-Loan vs Non-Cash (Billions €)

10.00 200.00

has contributed to an increase of fees in both the

government and corporate space. 5.00 150.00

-

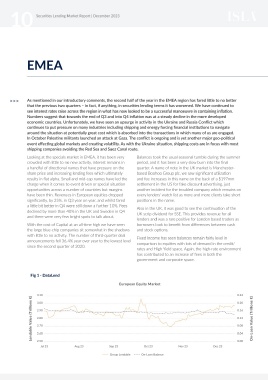

Fig 1 - DataLend Jan 23 Feb 23 Mar 23 Apr 23 May 23 Jun 23 Jul 23 100.00

European Equity Market Group Balance vs Cash Group Balance vs Non Cash

3.10 0.24

Lendable Value (Trillions €) 2.90 0.16 On-Loan Value (Trillions €)

0.20

3.00

2.80

0.12

2.70

0.08

2.60

0.00

2.50

Jul 23 Aug 23 Sep 23 Oct 23 Nov 23 Dec 23 0.04

Group Lendable On-Loan Balance