Page 12 - Securities_Lending_Market_Report_-_June_2022

P. 12

12 13

Securities Lending Market Report | June 2022

Fixed Income

>>> North America Fixed Income

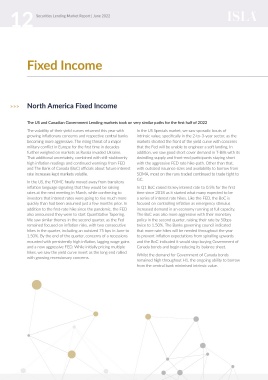

The US and Canadian Government Lending markets took on very similar paths for the first half of 2022 Fig 3 - S&P Global

The volatility of their yield curves returned this year with In the US Specials market, we saw sporadic bouts of

growing inflationary concerns and respective central banks intrinsic value, specifically in the 2-to-3-year sector, as the North American Government Bonds Cash vs Non-Cash

becoming more aggressive. The rising threat of a major markets shorted the front of the yield curve with concerns

military conflict in Europe for the first time in decades that the Fed will be unable to engineer a soft landing. In 640.00

further weighed on markets as Russia invaded Ukraine. addition, we saw good short cover demand in T-Bills with its 340.00

That additional uncertainty, combined with still-stubbornly dwindling supply and front-end participants staying short 330.00 620.00

high inflation readings and continued warnings from FED with the aggressive FED rate hike-path. Other than that, 320.00 600.00

and The Bank of Canada (BoC) officials about future interest with outsized issuance sizes and availability to borrow from 310.00 580.00

rate increases kept markets volatile. SOMA, most on the runs traded continued to trade tight to On-Loan vs Cash (Billions €) 350.00 560.00 On-Loan Value (Billions €)

300.00

GC. 290.00

In the US, the FOMC finally moved away from transitory 540.00

inflation language signaling that they would be raising In Q1 BoC raised its key interest rate to 0.5% for the first 280.00 520.00

rates at the next meeting in March, while confirming to time since 2018 as it started what many expected to be 270.00

investors that interest rates were going to rise much more a series of interest rate hikes. Like the FED, the BoC is 260.00 Feb 2022 Mar 2022 Apr 2022 May 2022 Jun 2022 500.00

Jan 2022

quickly than had been assumed just a few months prior. In focused on controlling inflation as emergency stimulus

addition to the first-rate hike since the pandemic, the FED increased demand in an economy running at full capacity. Group Balance vs Cash Group Balance vs Non Cash

also announced they were to start Quantitative Tapering. The BoC was also more aggressive with their monetary

We saw similar themes in the second quarter, as the Fed policy in the second quarter, raising their rate by 50bps

remained focused on inflation risks, with two consecutive twice to 1.50%. The Banks governing council indicated

hikes in the quarter, including an outsized 75 bps in June to that more rate hikes will be needed throughout the year

1.50%. By the end of the quarter, concerns of a recessions to prevent inflation expectations from spiralling upwards

mounted with persistently high inflation, lagging wage gains and the BoC indicated it would stop buying Government of

and a now aggressive FED. While initially pricing multiple Canada bonds and begin reducing its balance sheet.

hikes, we saw the yield curve invert as the long end rallied Whilst the demand for Government of Canada bonds

with growing recessionary concerns. remained high throughout H1, the ongoing ability to borrow

from the central bank minimised intrinsic value.