Page 10 - 2516_21_June_ISLA_Market_Report_-_March_2022_final

P. 10

10 11

Securities Lending Market Report | March 2022

Fixed Income

HQLA

As expected, we saw increased supply within the global government bond market in 2021.

Excess liquidity from quantitative easing across developed There was a general reduction of cross-currency spreads,

markets continued to hit new highs, suppressing curves and as central bank policy became synchronised globally and

also leading to collateral shortages. With record deposit risk appetite away from the security of the US dollar was

levels, banks became liability constrained. This problem reinvigorated.

was most obvious in the US, where the overnight reverse After an initial sell-off, yield curves remained flat for the

repurchase facility hit an all-time high of $1.9 trillion on majority of 2021, offering limited reinvestment opportunity,

31 December, as excessive cash and reduced collateral although curves became fractured into Q4 as central banks

availability supressed international discount margin rates. signalled imminent tapering and expectations of interest rate

rises intensified.

>>> Europe >>> US

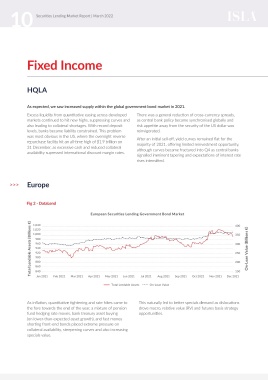

Fig 2 - DataLend Fig 3 - IHS Markit

European Securities Lending Government Bond Market 400 3.00 North American Securities Lending Government Bond Market 0.95

Total Lendable Assets (Billions €) 1,000 350 On-Loan Value (Billions €) Total Lendable Assets (Trillions €) 2.50 0.90 On-Loan Value (Trillions €)

1,040

1,020

980

0.85

2.00

960

300

1.50

0.80

940

920

250

0.75

1.00

900

880

200

.50

0.70

860

0.65

-

150

840

Jun 2021

May 2021

Jan 2021

Feb 2021

Mar 2021

Aug 2021

Jun 2021

May 2021

Apr 2021

On-Loan Balance

Total Lendable Assets Jul 2021 On-Loan Value Sep 2021 Oct 2021 Nov 2021 Dec 2021 Jan 2021 Feb 2021 Mar 2021 Apr 2021 Total Lendable Assets Jul 2021 Aug 2021 Sep 2021 Oct 2021 Nov 2021 Dec 2021

As inflation, quantitative tightening and rate hikes came to This naturally led to better specials demand as dislocations In the US, the ongoing impact of the global pandemic shifted to rising inflation, the front end of the curve started

the fore towards the end of the year, a mixture of pension drove macro, relative value (RV) and futures basis strategy appears to have had a significant impact on yield curves, to sell aggressively, dropping on economic and central

fund hedging rate moves, bank treasury asset buying opportunities. which remained relatively muted and flat through 2021. bank expectations. These curve movements coincided with

(on lower-than-expected asset growth), and fast money The year started with the vaccine rollout, which caused specials opportunities for most agent lenders.

shorting front-end bonds placed extreme pressure on a sharp sell-off in the 5-30 sector United States Treasury

collateral availability, steepening curves and also increasing bonds (USTs) and sent the yield curve steeper, particularly

specials value.

through 10-year. However, as the year elapsed and focus