Page 10 - 2516_21_June_ISLA_Market_Report_-_Aug_2023_-_final

P. 10

10 11

Securiti es Lending Market Report | June 2023

Equiti es

>>> EMEA

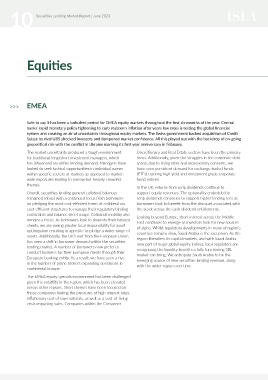

Safe to say it has been a turbulent period for EMEA equity markets throughout the fi rst six months of the year. Central Fig 1 - DataLend

banks’ rapid monetary policy ti ghtening to curb stubborn infl ati on aft er years low rates is testi ng the global fi nancial

system and creati ng an air of uncertainty throughout equity markets. The Swiss government backed acquisiti on of Credit European Equity Market

Suisse by rival UBS shocked investors and dampened market confi dence. All this played out with the backdrop of on-going

geopoliti cal risk with the confl ict in Ukraine marking its fi rst year anniversary in February. 3.00 0.30

The market uncertainty produced a tough environment Discreti onary and Real Estate sectors have been the primary 2.95 0.25

for traditi onal long/short investment managers, which focus. Additi onally, given the struggles in the corporate debt 2.90

has infl uenced securiti es lending demand. Managers have space, due to rising rates and recessionary concerns, we 2.85 0.20

looked to seek tacti cal opportuniti es in individual names have seen persistent demand for exchange traded funds Lendable Value (Trillions €) 2.80 0.15 On-Loan Value (Trillions €)

2.75

within specifi c sectors or markets as opposed to market- (ETFs) tracking high yield and investment grade corporate 2.70 0.10

wide exposures leading to narrow but heavily crowded bond indices. 2.65

themes. 0.05

In the UK, returns from scrip dividends conti nue to 2.60

Overall, securiti es lending general collateral balances support equity revenues. The opti onality embedded in 2.55 0.00

remained robust with a conti nued focus from borrowers scrip dividends conti nues to support higher lending fees as Jan 2023 Feb 2023 Mar 2023 Apr 2023 May 2023 Jun 2023

on pledging the most cost-effi cient forms of collateral via borrowers look to benefi t from the discount associated with Group Lendable On-Loan Balance

cost-effi cient structures to manage their regulatory binding the stock versus the cash dividend enti tlements.

constraints and balance sheet usage. Collateral mobility also Looking beyond Europe, short interest across the Middle

remains a focus. As borrowers look to diversify their balance East conti nues to emerge as investors look for new sources

sheets, we are seeing greater local responsibility for asset of alpha. Whilst regulatory developments in many of region’s

opti mizati on resulti ng in appeti te to pledge a wider range of countries remains slow, Saudi Arabia is the excepti on. As the Fig 2 - DataLend

assets. Additi onally, the UK‘s exit from the European Union region liberalizes its capital markets, and with Saudi Arabia European Equity Market Cash vs Non-Cash

has seen a shift in borrower demand within the securiti es now part of major global equity indices, local regulators are

lending market. A number of borrowers now prefer to recognizing the liquidity benefi ts a fully functi oning SBL

conduct business for their European clients through their market can bring. We anti cipate Saudi Arabia to be the 70.00 250.00

European banking enti ty. As a result, we have seen a rise emerging source of new securiti es lending revenue, along 60.00 200.00

in the number of prime brokers expanding operati ons in with the wider region over ti me. 50.00

conti nental Europe. 40.00 150.00

The EMEA equity specials environment has been challenged On-Loan vs Cash (Billions €) 30.00 100.00 On-Loan vs Non-Cash (Billions €)

given the volati lity in the region, which has been elevated 20.00

versus other regions. Short themes have been focused on 10.00 50.00

those companies feeling the pressures of high interest rates,

infl ati onary cost of raw materials, as well as a cost-of-living 0.00 Feb 2023 Mar 2023 Apr 2023 May 2023 Jun 2023 0.00

Jan 203

crisis impacti ng sales. Companies within the Consumer

Group Balance vs Cash Group Balance vs Non-Cash