Page 18 - 2516_21_June_ISLA_Market_Report_-_Dec_2022

P. 18

18 19

Securities Lending Market Report | December 2022

>>> Fixed Income

In H2 2022, North American markets continued to face rising interest rates, worries surrounding inflation and a possible

recession. Escalating geopolitical tensions and structural market events in the form of coordinated central bank policy combined

to increase volatility across US markets.

Central Banks globally continued their coordinated tightening of monetary policy throughout the second half of 2022. Elevated

inflation and a robust labour market garnered market attention and presented substantial volatility in the financial markets. Demand

for High Quality Liquid Assets (HQLA) and collateral transformation remained in the spotlight. However, late summer and early

fall witnessed the short-end of the Treasury financing curve trade almost entirely special on the back of large federal fund rate

increases. Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NSFR) and Uncleared Margin Rules (UMR) combined with

reduced Treasury issuance and Quantitative Tightening (QT) kept US Treasury demand and utilisation firm. While the specialness of

short-coupons and Treasury Bills has abated, collateral transformation remains highly sought after in the market.

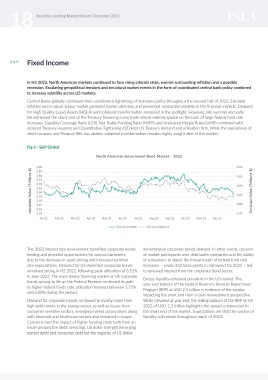

Fig 6 - S&P Global

North American Government Bond Market - 2022

2.90 0.90

Lendable Value (Trillions $) 2.75 0.90 On-Loan Value (Trillions $) Demand for corporate bonds continued to

2.85

2.80

0.95

2.70

2.65

2.60

mostly come from high yield names in the

0.85

2.55

2.50

0.80

2.45

2.40

2.35

sensitive sectors, emerging market corporations

Jan 22 Feb 22 Mar 22 Apr 22 May 22 Jun 22 Jul 22 Aug 22 Sep 22 Oct 22 Nov 22 Dec 22 0.75 energy sector, as well as issues from consumer

along with financials and healthcare sectors also

Group Lendable On-Loan Balance

remained in scope.

The 2022 interest rate environment benefited corporate bonds denominated corporate bonds demand. In other words, concern

lending and provided opportunities for various borrowers, of market participants over debt laden companies and the ability

due to the decrease in asset pricing and increased terminal of consumers to digest the forward path of federal fund rate

rate expectations. Demand for US domiciled corporate bonds increases – nearly 350 basis points in retrospect for 2022 – led

remained strong in H2 2022, following peak utilisation of 6.51% to renewed interest from the corporate bond sector.

in June 2022. The once sleepy financing market of US corporate Excess liquidity remained prevalent in the US market. The

bonds sprung to life as the Federal Reserve continued its path year-end balance of the Federal Reserve’s Reverse Repurchase

to higher federal funds rate, utilisation hovered between 5.75% Program (RRP) at USD 2.5 trillion is evidence of the surplus

and 6.00% during the period.

impacting the short end from a cash reinvestment perspective.

Demand for corporate bonds continued to mostly come from While elevated at year end, the rolling balance of the RRP in H2

high yield names in the energy sector, as well as issues from 2022 of USD 2.2 trillion highlights the spread compression in

consumer sensitive sectors, emerging market corporations along the short end of the market. Expectations are that the surplus of

with financials and healthcare sectors also remained in scope. liquidity will remain throughout much of 2023.

Concerns over the impact of higher funding costs both from an

issuer perspective (debt servicing), US dollar strength (emerging

market debt) and consumer debt led the majority of US dollar