Page 11 - ISLA_SLReport_Feb2020_spreads

P. 11

Global Market Dynamics Set against something of a mixed economic and geopo- to €21 trillion, an increase of some 7% over the six month

period to 31 December 2019. Over the same period, the

litical backdrop, and as discussed earlier in this review,

securities lending revenues in 2019 reflected these same DJIA increased in value by an estimated 6.8%, suggesting

uncertainties. It is worth noting however, that although most if not all of the increase in the value of securities

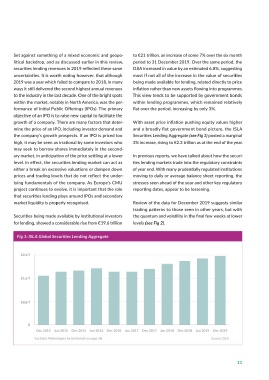

2019 was a year which failed to compare to 2018, in many being made available for lending, related directly to price

ways it still delivered the second highest annual revenues inflation rather than new assets flowing into programmes.

to the industry in the last decade. One of the bright spots This view tends to be supported by government bonds

within the market, notably in North America, was the per- within lending programmes, which remained relatively

formance of Initial Public Offerings (IPOs). The primary flat over the period, increasing by only 3%.

objective of an IPO is to raise new capital to facilitate the

growth of a company. There are many factors that deter- With asset price inflation pushing equity values higher

In many ways, 2019 was something of an investment are preferring to leave that money at the Fed rather than mine the price of an IPO, including investor demand and and a broadly flat government bond picture, the ISLA

conundrum, as investors shrugged off trade tensions invest liquidity in the repo markets. the company’s growth prospects. If an IPO is priced too Securities Lending Aggregate (see Fig 1) posted a marginal

and warnings of a global slow down by pushing markets high, it may be seen as irrational by some investors who 3% increase, rising to €2.3 trillion as at the end of the year.

towards their best year since the end of the financial cri- As liquidity becomes more prominent in the context of may seek to borrow shares immediately in the second-

sis a decade ago. systemic risk, this raises important questions for secu- ary market, in anticipation of the price settling at a lower In previous reports, we have talked about how the securi-

rities lending. Albeit for subtly different reasons, we can level. In effect, the securities lending market can act as ties lending markets trade into the regulatory constraints

The MSCI World Index, which tracks stocks across the see clearly how an absence of liquidity can fundamentally either a break on excessive valuations or dampen down of year end. With many prudentially regulated institutions

developed world jumped by almost 24% during 2019, its undermine the operation of the government bond repo prices and trading levels that do not reflect the under- moving to daily or average balance sheet reporting, the

strongest performance since 2009. A surge in US tech- markets. Securities markets are in many ways no differ- lying fundamentals of the company. As Europe’s CMU stresses seen ahead of the year and other key regulatory

nology giants combined with a strong recovery in Asian ent. The provision of trading liquidity to market mak- project continues to evolve, it is important that the role reporting dates, appear to be lessening.

stocks and the Eurozone, drove the rally. ers through access to securities lending, allows them to that securities lending plays around IPOs and secondary

actively make two-way prices in securities without nec- market liquidity is properly recognised. Review of the data for December 2019 suggests similar

As commentators have looked more closely at the driv- essarily holding them as inventory. If Europe is to push trading patterns to those seen in other years, but with

ers behind this resurgence however, questions about ahead with its ambitious plans to develop a fully autono- Securities being made available by institutional investors the quantum and volatility in the final few weeks at lower

its sustainability have been raised. It would appear that mous capital markets framework, the broader participa- for lending, showed a considerable rise from €19.6 trillion levels (see Fig 2).

investors are increasingly immune to poor economic data, tion of institutional investors, including UCITS funds will

as they see it as a signal for more central bank interven- be of critical importance. Fig 1: ISLA Global Securities Lending Aggregate

tion pushing liquidity into the markets and inflating asset

prices further. As central banks are increasingly active in Strong equity market performance, combined with the

the money markets, many have described this as ‘stealth political uncertainties around Brexit and the ongoing €2.4 T

Quantitative Easing (QE)’. It has been suggested by some trade spat between the US and China, appeared to lead to

that by the end of January, the Fed’s balance sheet will a loss of conviction in and around the alternative invest-

surpass what it was at the height of the vast QE program ment communities. Market level data provided by the €1.6 T

instigated after the global financial crisis in 2008. Alternative Investment Management Association (AIMA)

indicated that alternative managers saw net outflows

The other factor that is cited by many commentators is across all investment strategies in the first three quar-

the post-crisis regulatory regime that is designed to curb ters of 2019. The Sharpe Ratio which indicates how well €0.8 T

risk taking and thereby disincentivise banks to support a particular asset or a given portfolio’s return compen-

trading liquidity, particularly across critical regulatory sates for the risk taken by the investor, also fell across the

reporting dates. alternative investment sector in the first nine months of 0

2019. This suggests that some of these outflows could be Dec 2014 Jun 2015 Dec 2015 Jun 2016 Dec 2016 Jun 2017 Dec 2017 Jun 2018 Dec 2018 Jun 2019 Dec 2019

Quite simply, as large banks have more than enough connected with either a slowing of returns or an increase *see Data Methodogies for full details on page 36 Source: ISLA

excess liquidity to meet regulatory requirements, they of risk within various strategies.

10 11