Page 25 - ISLA_SLReport_Feb2021_final

P. 25

We have explored some of the reasons behind these Another factor that would have contributed to the

Utilisation, as measured using the value of securities these numbers. The following chart that looks at the types of trading patterns before. Over the past two to reported 10% fall in cash collateralised business in

on-loan, steadily increased over the period, rising split between cash and non-cash collateral highlights three years, much of the demand to borrow high quality the final two weeks of the year, would have been the

from €1 trillion to over €1.1 trillion at the year-end. how balances against non-cash collateral strengthened government bonds or High-Quality Liquid Assets (HQLA), underlying short-term cash markets. As banks and other

However, behind what appears to have been a broadly into the year-end, whilst those loans that were secured has been driven by borrowers’ desire to secure HQLA institutions look to shrink their balance sheets over the

strengthening on-loan position (especially into the year- against cash collateral fell away steeply in the final few for extended periods. If a prudentially regulated entity year-end, the market for short term cash investments

end), there were clearly several factors in play behind days of the year.

is able to borrow an eligible HQLA asset for periods of can almost disappear. Therefore, many lenders who are

three months or more, they can include these assets in the in receipt of cash collateral prefer to recall the associated

calculation of their Liquidity Coverage Ratio (LCR), which loan positions, and effectively return the cash to the

requires banks to hold sufficient HQLA to provide a robust borrower (as they don’t want to assume the reinvestment

liquidity cushion for the organisation during periods of risk during this time).

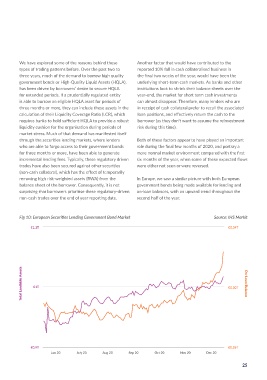

Fig 9: Global Securities Lending Government Bond Market (Cash vs Non-Cash) Source: IHS Markit market stress. Much of that demand has manifested itself

through the securities lending markets, where lenders Both of these factors appear to have played an important

€0.27T €1T who are able to forgo access to their government bonds role during the final few months of 2020, and portray a

for three months or more, have been able to generate more normal market environment compared with the first

incremental lending fees. Typically, these regulatory driven six months of the year, when some of these expected flows

trades have also been secured against other securities were either not seen or were reversed.

(non-cash collateral), which has the effect of temporarily

removing high risk-weighted assets (RWA) from the In Europe, we saw a similar picture with both European

balance sheet of the borrower. Consequently, it is not government bonds being made available for lending and

surprising that borrowers prioritise these regulatory-driven on-loan balances, with an upward trend throughout the

€0.26T €0.9T

non-cash trades over the end of year reporting date. second half of the year.

Fig 10: European Securities Lending Government Bond Market Source: IHS Markit

On-Loan Balance vs Cash €0.25T €0.8T On-Loan Balance vs Non Cash €1.1T €0.34T

Total Lendable Assets On-Loan Balance

€0.24T €07T €1T €0.30T

€02.3T €0.6T

€0.9T €0.26T

Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20 Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20

24 25