Page 26 - ISLA_SLReport_Feb2021_final

P. 26

3% 3%

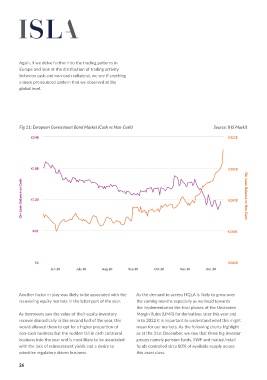

Again, if we delve further into the trading patterns in

Europe and look at the distribution of trading activity 6%

between cash and non-cash collateral, we see if anything

a more pronounced pattern that we observed at the

global level.

28% Fig 12: Global Government Bond 27%

Lendable Supply by Fund Type

Source: DataLend

Fig 11: European Government Bond Market (Cash vs Non-Cash) Source: IHS Markit 2%

9% 8%

€24B €320B

8%

24%

€18B €300B Fig 13: Global Government Bonds

On-Loan by Fund Type 31%

On-Loan Balance vs Cash €12B €280B On-Loan Balance vs Non Cash Banks/Broker Dealers

Source: DataLend

30%

Corporations/LLP/LLC

Foundation/Endowment

Government/Sovereign Entities/Central Banks

Insurance Companies 15% 5%

Mutual/Retail Funds

€6B €260B

Pension Plans

Undisclosed/Other

€0 €240B

Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20

We have in the past highlighted the importance of the This potential sensitivity is underlined when we look at

SWF sector to this market, however pension funds and current on-loan balances, where pension plans make up

Another factor in play was likely to be associated with the As the demand to access HQLA is likely to grow over retail funds still account for 28% and 24% respectively of circa 30% of all open loans as at 31 December. Conversely,

recovering equity markets in the latter part of the year. the coming months especially as we head towards all available supply. retail funds including UCITS are typically underweight

the implementation the final phases of the Uncleared in terms of on-loan balances, with their proportion of

As borrowers saw the value of their equity inventory Margin Rules (UMR) for derivatives later this year and As these institutions, who have traditionally made their active trades at 15% compared to their 24% of available

recover dramatically in the second half of the year, this in to 2022 it is important to understand what this might government bonds available for lending think about their inventory. Continued regulatory restrictions around

would allowed them to opt for a higher proportion of mean for our markets. As the following charts highlight UMR obligations, we may see these firms reprioritise their UCITS in particular, have led borrowers to opt to borrow

non-cash business but the sudden fall in cash collateral as at the 31st December, we saw that three big investor use away from lending, thereby reducing overall availability. government bonds from both SWFs and pension funds,

business into the year end is most likely to be associated groups namely pension funds, SWF and mutual/retail where they see more flexibility around factors such

with the lack of reinvestment yields and a desire to funds controlled circa 80% of available supply across This could have implications over time for overall market as collateral requirements and the provision of term

prioritise regulatory driven business. this asset class. liquidity and pricing. transactions particularly around LCR driven trades.

26 27