Page 9 - ISLA_SLReport_Sep2019

P. 9

On 5 August 2019, stocks plunged on Wall Street as the Whilst equity markets experienced strong growth through

Dow Jones Industrial Average sank by more than 766 the first quarter of 2019, hedge funds were slow to re

points (2.9%) – its worst trading day of the year – and the deploy capital, both on the long and on the short side.

S&P 500 and Nasdaq both fell 3% and 3.4% respectively This conservatism prevailed through the first quarter of

amid fears that the trade war was intensifying. London the year, with uncertainty relating to a number of key

listed shares on the FTSE 100 fell by circa 180 points, macro factors including global trade wars, Brexit and

almost 2.5% following steep losses on Asian markets, central bank policy; all negatively impacting investment

again reflecting the global uncertainties around the future conviction. As a result, hedge fund leverage levels and

direction of trading relations between the world’s largest gross equity market exposures remained suppressed.

two economies. Whilst reports suggest this improved modestly in

the second quarter of the year, strong equity market

Closer to home, the risks associated with the way in performance meant hedge funds typically looked to

which the UK will leave the European Union (EU) have maintain a net long bias, which negatively impacted

intensified. In recent weeks, the change of UK Prime global securities lending volumes.

Minister has led to a very different stance from the UK.

Although it remains to be seen as to how this plays out Not surprisingly, the combination of some very challenging

in terms of the separation from the EU, in the short-term geo-political and increasingly difficult economic

markets are pricing further uncertainty, with sterling headwinds have begun to come through in bottom line

trading at all-time lows in the currency markets. performance across our industry. Data published recently

by IHS Markit suggested that global revenues from

A constant theme that we saw in 2018 and into 2019, was securities lending for the first six months of 2019, down

one of uncertainty which not unexpectantly has led to some 15% at €4.5 billion, compared to the same period

varied investor sentiments, and at times inactivity. Ahead last year. Revenue streams still come predominantly from

of the year end, we saw significant de-risking by hedge equities securities lending, which represent circa 80% of

funds which was precipitated by a rise in equity market gross revenues globally. Conversely and notwithstanding

volatility, and meant that most hedge funds started 2019 the high volumes of government bonds being lent today,

in a risk-off or neutral position. they only account for 15% of global revenues.

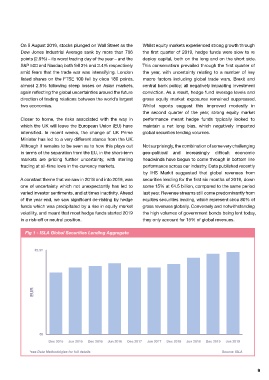

Fig x - ISLA Securities Lending Aggregate

Fig 1 - ISLA Global Securities Lending Aggregate

€2.3T

Global Market Dynamics

Many of the factors that created the geo-political and After strong growth in 2017 and early 2018, global

economic backdrop to the first six months of 2019, were economic activity slowed in the second half of last

very familiar to those observers who had watched events year, reflecting a confluence of factors affecting major EUR

unfold in 2018. economies. China’s growth declined following a

combination of needed regulatory tightening to rein in

As these factors played out more broadly into financial shadow banking, and an increase in trade tensions with

markets, we saw knock-on effects into areas of investment the United States. These trade tensions have, if anything,

management and in the provision of market liquidity, both increased in the past few weeks, and at the time of

linking directly to the demand to borrow securities. This in writing, financial markets around the world have seen €0

turn changed some of the economics around our markets, sharp falls amid growing fears that the US-China trade Dec 2015 Jun 2015 Dec 2016 Jun 2016 Dec 2017 Jun 2017 Dec 2018 Jun 2018 Dec 2019 Jun 2019

leading to a depressed revenue picture for the first half of dispute could escalate into a full-scale currency war, with

*see Data Methodolgies for full details Source: ISLA

the year. More on this later. damaging consequences for the world economy.

8 9