Page 9 - 2822_24_Apr_ISLA_Manifesto_political_narrative_-_digital_version_7

P. 9

ISLA MANIFESTO 2024

9

What is Securities

Lending & Borrowing? From a legal and tax perspective, it is important to note that:

• Most transactions are carried out using ‘outright transfer of title’ meaning that

legal title to both securities and collateral passes on to the borrower and the lender

respectively.

Securities lending and borrowing is a long-

established and well-functioning market in Europe, • However, whilst legal ownership to the securities is transferred to the borrower

where an investor temporarily lends securities throughout the duration of the transaction, the economic ownership remains with

the lender. Whilst the borrower receives all dividends and/or interest coupons

to a borrower, in return for a fee. It is one of four during the life of the transaction, these are then passed back to the lender, via what

different securities financing transaction (SFT) types, is called a manufactured payment.

along with repurchase transactions (repos), buy- • Most transactions take place under the Global Master Securities Lending

sell back transactions, and margin or commodity Agreement (GMSLA) - Title Transfer and the Security Interest over Collateral

lending. 7 (Pledge) Agreement both supported by legal opinions with regards to the

Securities can be in the form of bonds issued by enforceability of the agreement across jurisdictions.

governments or corporates as well as equities and

Exchange-Traded Funds (ETFs). In addition to the Click here to access the ISLA

fee, the borrower provides the lender with collateral Securities Lending & Borrowing Hub Supply Demand

in the form of cash or other securities. This protects

the lender from the risk of potential loss if the with a medium to long-term horizon and thus do not

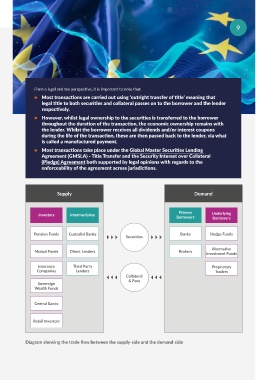

borrower becomes insolvent and is unable to return need access to all of their securities on a daily basis. Primary Underlying

the lender’s securities. The value of the collateral Investors Intermediaries Borrowers Borrowers

provided by the borrower is normally greater than By lending securities, they can receive additional

the value of the borrowed securities, providing income without losing the benefits attached to those Pension Funds Custodial Banks Banks Hedge Funds

additional protection for the lender. securities, such as dividends and interest payments. Securities

The revenue generated can help reduce costs for

To further protect both parties from market investors, retail and pension plans in Europe. Alternative

fluctuations during the life of the transaction, Mutual Funds Direct Lenders Brokers Investment Funds

securities and collateral on loan are revalued on a The European Central Bank (ECB) and other national

daily basis and adjusted if needed. At the end of the Central Banks (NCBs) also use securities lending as Insurance Third Party Proprietary

transaction the borrower and lender return their part of their monetary policy. This is vital for price Companies Lenders Collateral Traders

respective securities and collateral to one another. stability, economic growth in the Eurozone, financial Sovereign & Fees

Securities are frequently lent on an open basis and stability, as well as an autonomous EU capital Wealth Funds

as such, can be recalled if the lender requires the market, which lessens external dependence and

securities back. These requirements form part of provides sufficient resources internally for European Central Banks

market standard legal agreements and the processes businesses.

are further supported by widely accepted best Whilst only accounting for a relatively small part

practices between market participants. of the market, retail investors have also begun to Retail Investors

utilise securities lending for incremental income via

Lenders are usually investors such as pension funds,

mutual funds including UCITS, insurance funds and a range of trading platforms and aggregators (firms

Sovereign Wealth Funds (SWFs), that typically invest that combine small retail holdings into tradeable Diagram showing the trade flow between the supply-side and the demand-side

volumes).

7 According to ESMA’s report on “EU Securities Financing Transactions markets 2024”, the total outstanding exposure of SFTs is EUR 9.8tn, as

of September 2023. Repos account for EUR 6.7tn or 68% of the total, securities lending for EUR 2.3tn (23%), buy-sell back for EUR 743bn

(8%), and margin lending for EUR 124bn (1%).