Page 17 - 2516_21_June_ISLA_Market_Report_-_Aug_2023_-_final

P. 17

16 17

Securiti es Lending Market Report | June 2023

Fixed Income

>>> US Fixed Income

Rising infl ati on and subsequent global central bank interest rate increases have seen bond valuati ons decline, prompti ng

signifi cant shorti ng opportuniti es. In additi on, the ongoing war between Russia and Ukraine, alongside specifi c market risk

events, such as the US debt ceiling impasse, together with stresses in the global fi nancial sector, have resulted in signifi cant

fl ight-to-quality demand for the safest and most highly rated assets.

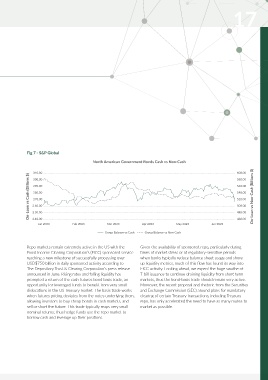

Fig 6 - S&P Global Fig 7 - S&P Global

North American Government Bond Market North American Government Bonds Cash vs Non-Cash

2.80 0.88 310.00 600.00

Lendable Value (Trillions $) 2.70 0.82 On-Loan Value (Trillions $) On-Loan vs Cash (Billions $) 2.60.00 560.00 On-Loan vs Non-Cash (Billions $)

0.86

300.00

580.00

2.75

0.84

290.00

2.65

280.00

540.00

0.80

520.00

2.60

270.00

0.78

500.00

2.55

0.76

2.50

460.00

2.40.00

0.72

2.45

Jan 2023 Feb 2023 Mar 2023 Apr 2023 May 2023 Jun 2023 0.74 2.50.00 Feb 2023 Mar 2023 Apr 2023 May 2023 Jun 2023 480.00

Jan 2023

Group Lendable On-Loan Balance Group Balance vs Cash Group Balance vs Non-Cash

This typically transpires in demand for sovereign debt, with US Treasuries also remain well-sought from an upgrade perspecti ve, Repo markets remain extremely acti ve in the US with the Given the availability of sponsored repo, parti cularly during

Treasuries the asset of choice. The Federal Reserve has lift ed with borrowing counterparti es seeking to improve regulatory Fixed Income Clearing Corporati on’s (FICC) sponsored service ti mes of market stress or at regulatory-sensiti ve periods

interest rates to 5.25-5.50%, driving signifi cant demand along capital positi ons by sourcing treasuries in term maturity reaching a new milestone of successfully processing over when banks typically reduce balance sheet usage and shore

the curve, and prompti ng specials acti vity in the most recently exposures versus equity and ETF collateral. Furthermore, USD$750 billion in daily sponsored acti vity according to up liquidity metrics, much of this fl ow has found its way into

issued bonds. Treasuries conti nue to be the most sought asset recent policy changes by the Bank of Japan prompted renewed The Depository Trust & Clearing Corporati on’s press release FICC acti vity. Looking ahead, we expect the huge swathe of

in the sovereign space, accounti ng for a large component of the appeti te to pledge Japanese Government bonds as collateral announced in June. Rising rates and falling liquidity has T-bill issuance to conti nue draining liquidity from short-term

top 10 revenue generati ng securiti es. To highlight, $570 million given widening cross-currency basis swap spreads. Diverging prompted a return of the cash-futures bond basis trade, an markets, thus the bond-basis trade should remain very acti ve.

was generated from Americas sovereign bonds in the fi rst interest rate policies between the Fed and other global central opportunity for leveraged funds to benefi t from very small Moreover, the recent proposal and rhetoric from the Securiti es

half, approximately 60% of sovereign earnings globally. More banks boosted these low-risk revenue opportuniti es for our dislocati ons in the US Treasury market. The basis trade works and Exchange Commission (SEC) around plans for mandatory

recently, the US Treasury has been replenishing its coff ers with lending clients. when futures pricing deviates from the notes underlying them, clearing of certain Treasury transacti ons, including Treasury

vast amounts of new Treasury bill issuance, resulti ng in specials allowing investors to buy cheap bonds in cash markets, and repo, has only accelerated the need to have as many routes to

acti vity in shorter-dated securiti es. sell or short the future. This trade typically reaps very small market as possible.

nominal returns; thus hedge funds use the repo market to

borrow cash and leverage up their positi ons.