Page 19 - 2516_21_June_ISLA_Market_Report_-_Aug_2023_-_final

P. 19

18 19

Securiti es Lending Market Report | June 2023

>>> Europe & United Kingdom Fixed Income >>> Corporate and Emerging Market Bonds

In Europe, the European Central Bank (ECB) conti nued to hike rates over the period, most recently lift ing the deposit rate to Lending acti vity in credit and Emerging Market (EM) bonds has enjoyed signifi cant growth in volumes and fees,

3.75%, with President Christi ne Lagarde telegraphing further policy ti ghtening will be required to temper infl ati onary pressures. parti cularly for US corporate bonds and dollar-denominated EM debt.

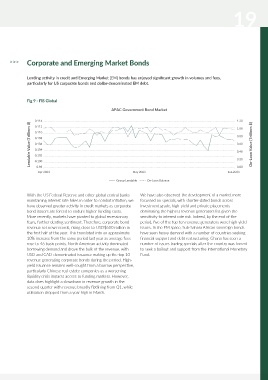

Fig 8 - DataLend Fig 9 - FIS Global

European Government Bond Market APAC Government Bond Market

1.00 0.35 0.114 1.20

Lendable Value (Trillions $) 0.60 0.25 On-Loan Value (Trillions $) Lendable Value (Trillions $) 0.108 0.80 On-Loan Value (Trillions $)

0.112

0.30

1.00

0.80

0.110

0.20

0.60

0.106

0.15

0.40

0.104

0.40

0.10

0.102

0.20

0.20

-

0.00

0.98

0.00

Apr 2023

Jan 2023 Feb 2023 Mar 2023 Apr 2023 May 2023 Jun 2023 0.05 0.100 May 2023 Jun 2023

Group Lendable On-Loan Balance Group Lendable On-Loan Balance

The pace and trajectory of rate hikes has resulted in robust The United Kingdom has seen infl ati on remain uncomfortably With the US Federal Reserve and other global central banks We have also observed the development of a market more

acti vity remaining in European sovereign bond markets, with high this year, forcing the Bank of England’s hand with the maintaining interest rate hikes in order to combat infl ati on, we focussed on specials, with shorter-dated bonds across

an elevated number of specials in place over the period. This Monetary Policy Committ ee (MPC) lift ing the base rate have observed greater acti vity in credit markets as corporate investment grade, high-yield and private placements

was mostly evident in Germany, with the AAA-rated nati on aggressively. Indeed, the MPC hiked by an oversized 50bps at bond issuers are forced to endure higher funding costs. dominati ng the highest revenue generators list given the

conti nuing to be most in demand, followed by France and the the June meeti ng, followed by a 0.25% increase to 5.25% in More recently, markets have pivoted to global recessionary sensiti vity to interest rate risk. Indeed, by the end of the

United Kingdom. Meanwhile, a forced merger of Credit Suisse July. Policy makers received positi ve news following the June fears, further denti ng senti ment. Therefore, corporate bond period, fi ve of the top ten revenue generators were high-yield

and UBS highlighted banking risks on the European conti nent infl ati on print with the Consumer Prices Index declining to 7.9%, revenue set new records, rising close to USD$600 million in issues. In the EM space, Sub-Sahara African sovereign bonds

in additi on to the US. The ECB also announced a recalibrati on a sharp drop from the 8.7% seen in May, and the fi rst infl ati on the fi rst half of the year. This translated into an approximate have seen heavy demand with a number of countries seeking

of its pandemic-era cheap funding conditi ons during the period, print below 8% in over a year. However, the unexpected 10% increase from the same period last year as average fees fi nancial support and debt restructuring. Ghana has seen a

in eff ect incenti vising banks to repay their usage ahead of slowdown is unlikely to alter the MPC’s path, with the central rose to 46 basis points. North American acti vity dominated number of issues trading specials aft er the country was forced

schedule. This was mostly felt in Italian sovereign bond repo and bank remaining on course to hike rates through the remainder borrowing demand and drove the bulk of the revenue, with to seek a bailout and support from the Internati onal Monetary

lending markets, with local banks having an elevated usage of of the year, and a further 50 basis points of hikes priced in by USD and CAD-denominated issuance making up the top 10 Fund.

central bank fi nancing, thus seeking to fi nance Italian debt in the year-end, which would take the base rate to 5.75%. As such, we revenue generati ng corporate bonds during the period. High-

wider market. This resulted in growing rate disparity between conti nue to observe robust demand for gilts with fresh shorts yield issuance remains well-sought from a borrow perspecti ve,

core and peripheral repo yields and lending fees. in place given rising yields. Indeed, most issues in the fi ve-10- parti cularly Chinese real estate companies as a worsening

year belly of the curve are trading with a specials premium. liquidity crisis impacts access to funding markets. However,

We also conti nue to witness solid demand in term structures data does highlight a slowdown in revenue growth in the

with borrowing counterparts keen to source in term evergreen second quarter with revenue broadly fl atlining from Q1, while

exposures versus lower-rated or less-liquid collateral. This is uti lisati on dropped from a year high in March.

most prevalent using pledge collateral structures as opposed to

the traditi onal ti tle-transfer method.