Page 19 - ISLA_SLReport_Feb2021_final

P. 19

extreme market volatility, fixed income ETFs were no Greater transparency coupled with inherent in-built standardisation was it also naturally limited scope and

longer the target for criticism. This newfound and welcome diversification makes ETFs an ideal collateral instrument consequently the initial Lists (one equity, one fixed income)

credibility will be the catalyst for further growth in use regardless of some of the current hurdles in understanding. ran to less than 100 ETFs and only grew organically to

without question. The development of industry standard metrics (i.e. , IHS around 120 in total due to the many inclusion constraints

there are now over 350 ETFs Markit ETF Lists v#1) increased understanding and built-in.

globally where the annualised Additionally the ongoing challenges in settling ETFs on a removed the traditional heavy lifting required in classifying

average lending revenue timely basis, (due to their multi-listed nature) - a particular the myriad of ETFs in existence. Consequently, the However’ as the chart below courtesy of BNY Mellon tri-

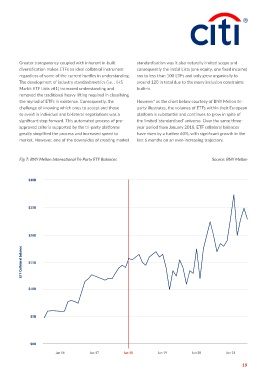

outweighs the cost of the sensitivity for overseas investors in regions such as Latin challenge of knowing which ones to accept and those party illustrates, the volumes of ETFs within their European

platform is substantial and continues to grow in spite of

America or Asia, has improved greatly by the growing

to avoid in individual and bi-lateral negotiations was a

ETF management fee harmonisation of the ICSD model – where irrespective of significant step forward. This automated process of pre- the limited ‘standardised’ universe. Over the same three-

listing, all ETFs settle in a centralised common depository approved criteria supported by the tri-party platforms year period from January 2018, ETF collateral balances

(Euroclear or Clearstream). Who knew that a little-known greatly simplified the process and increased speed to have risen by a further 60%, with significant growth in the

piece of Irish legislation – The Migration of Participating market. However, one of the downsides of creating market last 6 months on an ever-increasing trajectory.

This compares favourably to last time, when progress Securities Act 2019 – would be a welcome catalyst

was clearly more nascent. However many, if not all, of for European ETF market harmonisation? In addition

the previous impediments still remain – nomenclature to improving settlement rates, it ought to drive down Fig 7: BNY Mellon International Tri-Party ETF Balances Source: BNY Mellon

challenges, multiple sedols (due to cross-listings), market-maker costs, increase risk appetite, and harmonize

classification confusion (is it an equity, is it fixed income?) inventory pools - particularly important in helping grow

and perception inaccuracies (“nobody owns them” , secondary activities such as options on ETFs, which will $30B

“nobody wants them” , “they a retail product”) being just in turn fuel further long-term demand. We have already

some of the most common. The industry can and needs witnessed this in the United States, where an active

to do more to tackle these, particularly as many of the options market (in particular high-yield fixed income ETFs)

regulatory challenges and distractions it has had to face has driven demand to nearly 100% utilisation in certain

over the last few years have largely receded. There surely names and generated significant fee income. Interestingly, $25B

cannot be too many other opportunities where supply and there are now over 350 ETFs globally where the annualised

demand are growing in tandem by ‘at least 30%’ every average lending revenue outweighs the cost of the ETF

three years? If the industry can continue to develop new management fee – a substantial improvement from 2018

markets and push into new territories such as Romania, when there were 150 such products.³ $20B

one would hope it could similarly solve for the challenge of

having ETFs with multiple sedols?

Collateral – Now & Forward Looking

Fixed Income Adoption Perhaps now, much like three years ago, the collateral ETF Collateral balance $15B

aspect of ETFs has and continues to see the most

Three years ago, the use of ETFs by Fixed Income investors opportunity and advancement. The desire to pledge

was still a relatively new occurrence, they appreciated the ETFs as collateral, particularly in relation to the evolving $10B

benefits of going short as well as long, similar instruments, regulatory environment, is as strong as ever, and put simply,

but were often told the market (to borrow) didn’t exist. if more and more clients hold them (and in increasing

Undeterred hedge funds, and even traditional asset quantities) the need for greater acceptance as a collateral

managers, started using ETFs to tactically exploit segments instrument in their own right will only increase. Regulatory $5B

of the market and borrow demand grew steadily. What change in the form of MiFID II led to much greater

changed however was the industry reached a tipping point transparency on true European ETF trading volumes,

in adoption and ETFs are now an indispensable vehicle where OTC activity had traditionally accounted for

for Fixed Income investors both large and small. In fact, upwards of 70% of daily turnover and was largely invisible.

through the aftermath of the recent Covid pandemic, it $0B

became evident that unlike every previous period of ³Source: IHS Markit Jan 16 Jan 17 Jan 18 Jan 19 Jan 20 Jan 21

18 19