About ISLA

Regulation & Policy

Legal Services

Our Events

News & Insights

Status: Finalised Last Updated: 28/01/2022

Question:

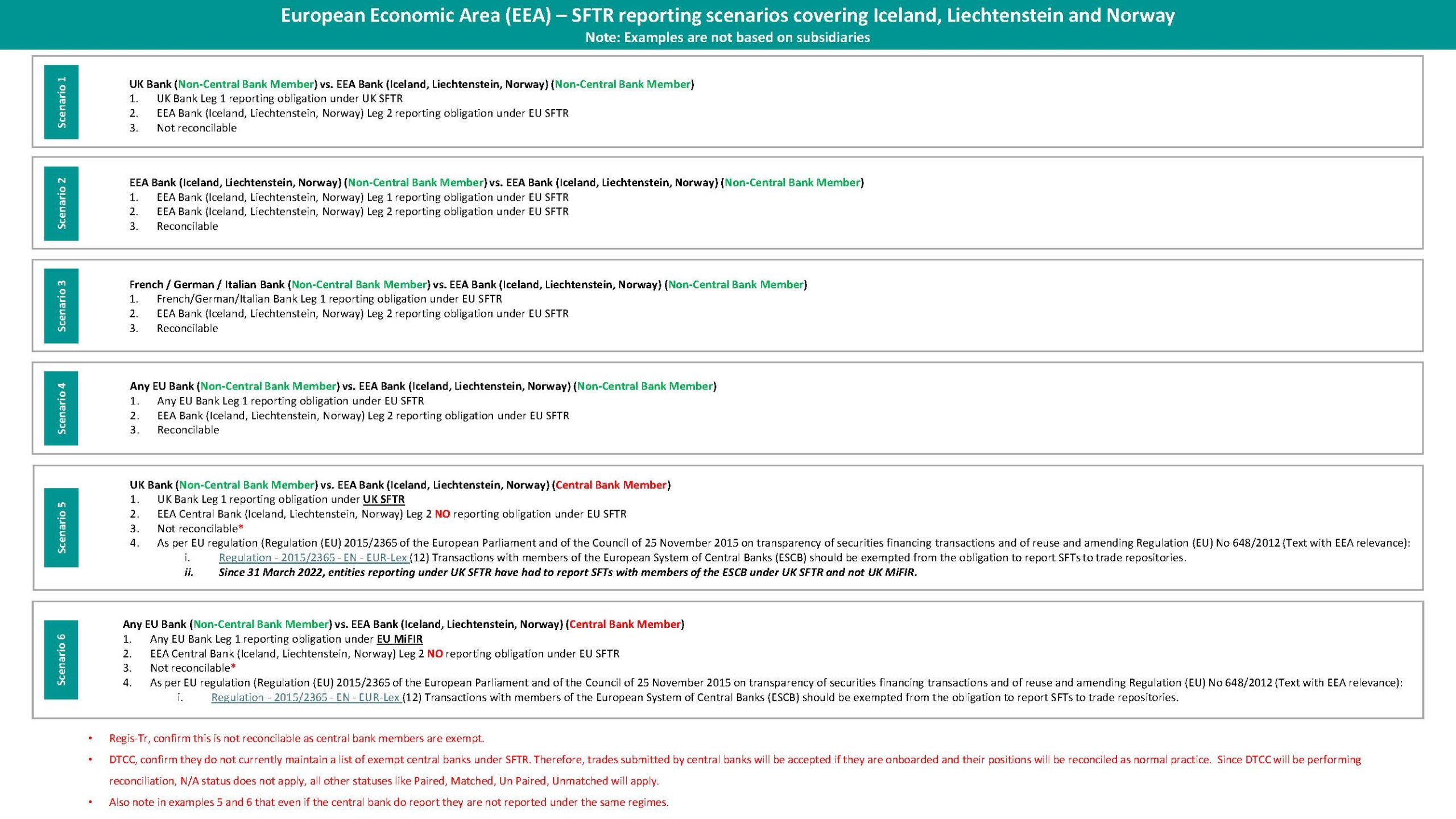

On https://www.efta.int/eea-lex/32015R2365 10 December 2021 the EEA Joint Committee agreed the adoption of Regulation (EU) 2015/2365 of the European Parliament

The EEA Joint Committee decision 385/2021 of 10 December 2021 notes that the Regulation shall apply from the date of entry into force of Decision of the EEA Joint Committee with the exception of Article 4(1) which shall apply over a phased period of 6 months for investment firms and credit institutions, 12 months for CCP and CSDs, and a further 15 months of other FC and NFCs.

Best Practice:

(SFTR-708)

Status: Finalised Last Updated: 28/09/2021

Question:

How should conditional and optional fields, as outlined within the validation rules, be interpreted?

Best Practice:

The population requirement of each validation type is outlined below as in the ‘general information’ tab of the SFTR validation rules for both EU and UK SFTR.

‘M’ – mandatory: the field is strictly required and validations of format and content are applied.

‘C’ – conditionally mandatory: Conditionally mandatory: the field is required if the specific conditions set out in the validation rules are met. If these conditions are not met, the field can be populated on an optional basis, unless clearly indicated that "Otherwise, the field shall be left blank". Format and content validations are applied

‘O’ – optional: the field shall be populated if applicable. Only format and content validations are applied when the field is populated.

‘-‘ – not applicable: the field shall be left blank

Where the information is pertaining to a field is known for conditional fields where the condition is not met and optional fields should be populated. This is important for reconciliations purposes. (SFTR-454)

Status: Finalised Last Updated: 28/09/2021

Question:

How should transactions with non-financial counterparties (NFCs) be reported under UK SFTR?

Best Practice:

In a written ministerial statement , the UK government confirmed that, as part of its onshoring process for SFTR, the UK will not implement the EU SFTR reporting obligation for NFCs.

Therefore, SFTs undertaken by UK participants with NFCs, will be reported as single sided under the UK SFTR regime. The reporting requirement for EU SFTR is unchanged, more information here.

For UK SFTR, Field 2.05 (Nature of the Reporting Counterparty) has been removed from the validation rules template. (SFTR-450)

Status: Finalised Last Updated: 26/04/2021

Question:

What are the reporting requirements for SFTR and MiFIR for UK and EU based firms?

Best Practice:

When the Brexit transition period ends, firms which are incorporated in the UK and EU will have their reporting obligation decoupled from one another. The result of this decoupling is that UK firms without a branch and UK branches of a 3rd country will cease to have a reporting requirement under EU SFTR and instead, will report their trades via UK SFTR which is regulated by the FCA. In cases where firms are UK based trading and via a branch within the EU, there is a double reporting requirement to report under both UK SFTR and EU SFTR. This decoupling also has implications for UTI exchange, more information regarding this can be found here.

In a written statement on June 23rd 2020, the UK Government confirmed that the reporting obligation for non-financial counterparties (NFCs) under EU SFTR would not be included within UK SFTR, therefore all NFCs that are UK operated, will not have a reporting requirement for SFTR.

ISLA have created a Excel tool based on our current understanding of the reporting requirement for financial counterparties (FCs) when transacting with each other in various cases. As well as the reporting requirements, the tool shows if the reporting is reconcilable (dual-sided), or not (single-sided). Find the reporting requirement tool here.

Please note: This tool is based on our current understanding of reporting requirements which may change prior to the end of the transition period. Find the latest information from the EU and the UK listed below.

Full ESMA statement regarding Brexit reporting for EU counterparties can be found here: Public Statement ESMA74-362-881

UK SFTR information including RTS, regulated by the FCA can be found here. (SFTR-441)

Status: Under Review Last Updated: 26/04/2021

Question:

Given that SFTR is based on EEA entities, should the ESCB exclusion also include the central banks of EEA countries who are not EU member states? (Central Bank of Iceland, Norges Bank, National Bank of Liechtenstein)

Best Practice:

See Level I text: REGULATION (EU) 2015/2365 – 25 November 2015 Article 2(2). Articles 4 and 15 do not apply to:

members of the European System of Central Banks (ESCB), other Member State’s bodies performing similar functions, and other Union public bodies charged with, or intervening in, the management of the public debt;

the Bank for International Settlements. Article 2(3). Article 4 does not apply to transactions to which a member of the ESCB is a counterparty. Members of the ESCB are excluded from SFTR. See below a full list of ESCB members, transactions with central banks outside of the ESCB should be included within SFTR Reporting.

(See here for more information regarding MiFID II requirement for ESCB transactions.)

European Central Bank

Austria: Oesterreichische National Bank

Belgium: National Bank of Belgium

Cyprus: Central Bank of Cyprus

Estonia: Eesti Pank

Finland: Bank of Finland

France: Banque de France

Germany: Deutsche Bundesbank

Greece: Bank of Greece

Ireland: Central Bank of Ireland

Italy: Bank of Italy

Latvia: Latvijas Banka

Lithuania: Bank of Lithuania

Luxembourg: Banque Centrale du Luxembourg

Malta Central: Bank of Malta

Netherlands: De Nederlandsche Bank

Portugal: Banco de Portugal

Slovakia: Národná banka Slovenska

Slovenia: Bank of Slovenia

Spain: Banco de Espana

Bulgaria: Bulgarian National Bank

Croatia: Croatian National Bank

Czech Republic: Czech National Bank

Denmark: Danmarks Nationalbank

Hungary: Magyar Nemzeti Bank

Poland: Narodowy Bank Polski

Romania: National Bank of Romania

Sweden: Sveriges Riksbank (SFTR-252)

Status: Finalised Last Updated: 26/04/2021

Question:

If trading with an EU Central Bank, is SFTR still required by the other participant in what has now effectively become a one-sided / non-matching reporting obligation?

Best Practice:

Under EU SFTR:

SFT activity, where the counterparty is a member of the European System of Central Banks (ESCB) is excluded from reporting under SFTR and must instead be reported via MiFIR. (See here for more information.)

SFTR activity, where the Counterpart is a Central Bank of a non-EU third country should be reported under SFTR in the normal way.

For further information on how to report ESCB lending under MiFID II, please see the summary document and reporting template example on how to report.

https://www.islaemea.org/regulation-and-policy/mifid-mifir/

Under UK SFTR:

Publication Notice 96. on 28/02/2022 – confirmed that SFTs with Bank of England should no longer be reported under MiFIR or SFTR, and transactions with any other central bank, ESCB or otherwise, will be reported under SFTR as a normal transaction effective from 01/04/2022.

https://www.fca.org.uk/publication/fca/handbook-notice-96.pdf (SFTR-166)

Status: Finalised Last Updated: 26/04/2021

Question:

If borrowing from a Small NFC through an Agent Lender, will the Agent Lender report on behalf of the Small NFC?

Best Practice:

The regulation passes the reporting obligation on to the borrower, rather than the agent lender, if they are an eligible, EU-domiciled, FC participant. Otherwise, the Small NFC has to perform this or allocate the task to a voluntary delegate.

See ISLA Best Practice SFTR-164 for further detail and references to ESMA Final Report and Guidelines.

(SFTR-248)

Status: Finalised Last Updated: 26/04/2021

Question:

Can ISLA confirm that they agree with AFME’s view and the RTS, as follows, that reporting Prime Brokerage (PB) loans is out-of-scope for reporting?

Regarding the reporting of prime brokerage (PB) client facing securities lending transactions under the SLB reporting template. ESMA understands the Margin Lending (ML) Short Market Value (SMV) reportable field to be equal to the amount of securities lending taking place under prime brokerage agreement.

AFME industry group has also confirmed that the ML SMV is proxy for reporting of Prime Broker client.

Note: SMV is not in fact always equal to the amount of securities lending, i.e. where the PB client over borrows beyond the SMV value of the short position taken in the market.

Best Practice:

ISLA is aligned with AFME’s understanding, where securities lending activity is conducted under a prime brokerage agreement (covering client’s short positions), that the following reference clarifies that this should be reported as part of a margin loan under SFTR.

See Guidelines Reporting under Articles 4 and 12 SFTR 06 January 2020 ESMA70-151-2838

190. The FSB requires the collection of data on short market value, which is the amount of securities lending taking place under prime brokerage agreement in order to cover the client’s short position(s). This short market value forms part of the portfolio on which the financing calculation is performed upon, and the securities loans made to a client are collateralised with the same portfolio used to collateralise margin loans extended to that same client. In order to avoid duplicated reporting, short market values should be reported together with margin loans, under the same UTI.

Firms need to satisfy themselves that in their individual circumstances the above applies, i.e. the method of execution/legal coverage is consistent with the above. What is clear is that ESMA do not want to see a duplication, so where members are reporting as SMV under the Margin Loan template, this is a very good indicator that you should not be reporting as individual SFTs under the Stock Borrow Loan template.

(SFTR-232)

Status: Finalised Last Updated: 26/04/2021

Question:

What happens in the case of a EU Small NFC trading with a Swiss Bank acting as a borrower in connection with reporting Field 1.03 (Reporting Counterparty) that needs a LEI from the reporting counterparty, if the Small NFC does not have a LEI (in case where an EU Small NFC lender delegates reporting to a Swiss bank),what would the Swiss bank report in that case?

Best Practice:

Please see best practice SFTR-164 which includes the legal opinion from Linklaters regarding third-country, mandatory, delegated reporting obligations.

Similarly to the United Kingdom, Switzerland are not mandatorily obliged assume delegate status when facing a EU SME-NFC within scope.

See Guidelines – Reporting under Articles 4 and 12 SFTR 06 January 2020 ESMA70-151-2838

60. Regarding SFTs concluded between an TC-FC outside the scope of application of SFTR (i.e. not covered by Article 2(1)(a)(ii) of SFTR) and an SME NFC , such SFTs should either be reported directly by the SME NFC to a TR, or otherwise make use of the possibility for delegation included in Article 4(2). (SFTR-227)

Status: Under Review Last Updated: 26/04/2021

Question:

Where an EEA broker dealer borrows from an undisclosed agent lender outside of the EEA, who has no regulatory obligation to provide beneficial owner breakdown and linked collateral allocation, how should this be reported?

Best Practice:

It is up to the commercial parties involved in the SFT to understand the status of their counterparties. If the non-EU agent lender or principle cannot or will not provide the data required for SFTR, for the EU reporting counterparty, then they will need to consider their commercial relationship and potentially stop trading with them.

For in-scope participants, reporting under SFTR is mandatory and not subjective. Out-of-scope participants will have to provide corresponding data for their counterparty to remain compliant with the regulators. See the following best practice for related information on non-EU participants and third-country counterparts (TCs) SFTR-171 (SFTR-204)

Status: Finalised Last Updated: 26/04/2021

Question:

What date does the SFTR reporting obligation go-live?

Best Practice:

Following the end of the scrutiny period on 13 March 2019, the full package of SFTR RTS and ITS has been published in the EU’s Official Journal.

In total, this consists of 10 different delegated and implementing regulations, including the relevant annexes.

The RTS and ITS will enter into force on 11 April 2019 (20th day after publication) and will then apply as follows:

11 July 2020: Reporting go-live for banks and investment firms (12 months after entry into force) -Delayed from the 11 April 2020 due to COVID-19.

11 July 2020: Reporting go-live for CCPs & CSDs (15 months after entry into force).

11 October 2020: Reporting go-live for the buy-side (18 months after entry into force).

11 January 2021: Reporting go-live for non-Financial Counterparties (NFCs) (21 months after entry into force). (SFTR-193)

Status: Finalised Last Updated: 10/08/2021

Question:

Is ‘mirroring’ at the TR technically possible; defined as a single file being transposed to create opposite and matching files?

Best Practice:

Most TRs offer a ‘mirroring’ service which is not a delegated, but an assisted reporting product.

Mirroring is defined as the transposition of the single file received, to create an opposite matching file from the counterparts’ perspective. Opposing fields that do not match and require a +/- are ‘flipped’, (i.e. Field1.03 (Reporting Counterparty), Field 1.09 (Counterparty Side), Field 1.11 (Other Counterparty)).

Participants should to speak to their TR or vendor to see if they can accommodate this process. (SFTR-173)

Status: Finalised Last Updated: 26/04/2021

Question:

If an in-scope NFC is trading with an out-of-scope participant who is not obliged to report under SFTR, whose responsibility does it become to report this transaction?

Whose responsibility is it to determine which counterparties are NFCs?

Who should determine when an NFC becomes an FC and therefore automatically stop reporting under the mandatory delegated report requirement?

Currently there is a mandatory delegated reporting act in place for SME-NFCs which passes the obligation to the counterparty in the SFT. What happens if their status changes when the stock is still on loan? Do they automatically reassume responsibility to report? Do they have to inform the counterparty that their status has changed? Or is this an annual event, declared only the authorities during the company returns.

If an in-scope NFC is trading with an out-of-scope participant and ordinarily therefore not obliged to report the SFT, whose responsibility does it become to report this transaction?

Is it our responsibility to work out which of our counterparties are NFC, or is it our counterparties responsibility to inform us?

Do we have to work out when an NFC becomes an NFC and therefore automatically stop reporting, or is it the counterparties responsibility to inform us?

Does Brexit change the mandatory delegation process?

Best Practice:

In the context of EMIR, there is an analogous situation, since a party may change from NFC+ to NFC- or vice versa. Following the changes in EMIR REFIT, a NFC needs (annually) to calculate whether it is above or below the clearing threshold, so once an entity has calculated it is NFC-, that determination remains good for the next 12 months.

As regards the party facing a NFC, the ESMA Q&As on EMIR indicate that representations should be obtained as to its status. If a NFC makes a representation that it is NFC+ or NFC-, the agreement under which such representation is made would usually impose an obligation on the NFC to notify the other party if its status changes – see for example ISDA’s Master Regulatory Disclosure Letter. Therefore, it should be possible to rely on the representation unless and until the NFC notifies that its status has changed. It is however possible that regulators would expect a financial counterparty to check from time to time whether the status of its NFC counterparty has changed, as part of more general KYC processes.

Turning to SFTR, whether a NFC is a SME (i.e. small NFC) is to be determined as at its balance sheet date, so if an entity was a small NFC at that date, it remains as such unless and until its next annual balance sheet is produced, even if, for example, its number of employees and turnover increases in the interim.

The MRRA caters for the Client representing, in the SFT Annex or elsewhere, that it is a small NFC. Once that representation has been made, the financial counterparty facing the small NFC could continue to rely on that representation, though as mentioned above, regulators may expect the FC periodically to refresh its information on the small NFC as part of general KYC processes.

If the small NFC ceases to be a small NFC, based on its most recent balance sheet, it would be in the interests of the FC to reclassify the NFC as soon as possible, because mandatory SFT reporting, and the attendant risk of liability, would cease to apply to the FC. In the draft MRRA, provision of an option for the reporting arrangement to switch automatically from mandatory reporting to delegated reporting once the NFC notifies the FC of its change of status (or, if so elected, the FC "otherwise becomes aware" of the change). However, if there are SFTs that were entered into when mandatory reporting applied, and still outstanding, that mandatory reporting would continue to apply to those transactions until terminated.

In the context of agency lending, the position is complicated since if the lender is a small NFC, and assuming the borrower is a FC, the mandatory reporting obligation will fall on the borrower.

If the lender ceases to be a small NFC then, for new transactions, mandatory reporting would cease to apply to the borrower, and presumably the lender would want to delegate its reporting obligation to the agent lender.

The position is also complicated by Brexit since, if a French small NFC lender lends to a UK borrower, in light of ESMA’s draft Guidelines para 5.3.2, once the UK has left the EU, the UK borrower (even if acting through a French branch) would not have any responsibility to report the transaction for the lender.

The MRRA does not cater for borrower having mandatory reporting obligation for small NFC lender and wanting to delegate the reporting to agent lender or (ii) small NFC ceasing to be small NFC and agent lender starting to report as delegate of NFC. These should be very rare scenarios.

ESMA Guidelines Reporting under Articles 4 and 12 SFTR: 06 January 2020

NFC should communicate with FC whether they qualify as small NFC or not, as well as update the FC on any potential changes in their status.

Regarding SFTs concluded between an TC-FC outside the scope of application of SFTR (i.e. not covered by Article 2(1)(a)(ii) of SFTR) and an SME NFC, such SFTs should either be reported directly by the SME NFC to a TR, or otherwise make use of the possibility for delegation included in Article 4(2).

When the SFT is concluded between two NFCs, both of them should report it to a TR, though they can make use of the possibility to delegate the reporting under Article 4(2) to one of them or to a third party.

A SME-NFC is defined as a small financial entity which is a legal entity with a balance sheet that does not exceed two of following three levels:

balance sheet total of EUR 20 million;

net annual turnover of EUR 40 million; and

average number of employees of 250. (SFTR-164)

Status: Finalised Last Updated: 26/04/2021

Question:

Article 4(1) of the Delegated Regulations for SFTR stated the requirement to backload SFTs that were still outstanding after the go-live of SFTR reporting. Following the delay to the initial go-live of SFTR, what are firms requirements for backloading transactions?

Best Practice:

On 19 March 2020, the European Markets and Securities Authority (ESMA) issued a statement that delayed the phase 1 implementation of SFTR. It accomplished this by expecting national competent authorities (NCAs) not to prioritise supervisory actions towards counterparties until July 2020 (phase 2 SFTR). This statement can be found here.

That statement has now been clarified further (ESMA revised statement 26 March 2020), specifically to address backloading, which is an SFTR requirement to capture data not required to be reported on go-live date. This statement can be found here.

ISLA’s understanding from ESMA’s statement is that all backloading will not be prioritised for all phases of SFTR, effectively allowing all firms to no longer consider backloading as a requirement. (SFTR-155)

Creating your PDF, please wait.

Sorry! You need to be logged in to access this document.

This premium content is available to ISLA member firms only. If you do not have a login, please use the ‘Request Login’ within the Member login.

If your firm is not a member of ISLA, find out more information regarding our current members, the types of membership we offer, and the benefits of joining.

Find out moreContent access not allowed

This content is not allowed on this membership level.

Change your membershipContent access not allowed

This content is not allowed on this membership level.

Change your membershipAlready a member? Login to your account

Interested in becoming a member?

ISLA’s members span the breadth and depth of the securities lending industry, and there are many benefits of joining the Association’s network.

Become a member today Securities Lending Best Practice

Securities Lending Best Practice