Page 10 - 2808_24_Jan_ISLA_Market_Report_-_Aug_2024

P. 10

10 11

Securities Lending Market Report | H1 2024

Government Bonds

>>> Global >>> European

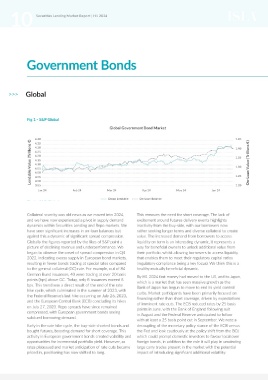

Fig 1 - S&P Global Fig 2 - S&P Global

Global Government Bond Market European Government Bond Market

4.40 1.45 1.32 390.00

Lendable Value (Trillions €) 4.25 1.35 On-Loan Value (Trillions €) Lendable Value (Trillions €) 1.26 370.00 On-Loan Value (Billions €)

4.35

1.30

380.00

4.30

1.40

1.28

4.20

360.00

4.15

1.24

4.10

350.00

1.30

1.22

4.05

340.00

4.00

1.20

1.25

3.95

3.90

1.16

3.85

320.00

Jan 24

Jan 24 Feb 24 Mar 24 Apr 24 May 24 Jun 24 1.20 1.18 Feb 24 Mar 24 Apr 24 May 24 Jun 24 330.00

Group Lendable On-Loan Balance Group Lendable On-Loan Balance

Collateral scarcity was old news as we moved into 2024, This removes the need for short coverage. The lack of On the euro side the market continues to focus on the The recent general lack of repo rate squeezes around the

and we have now experienced a pivot in supply demand excitement around futures delivery events highlights upcoming go-live of the ECB’s new operational framework cheapest-to-deliver futures delivery can be interpreted as

dynamics within Securities Lending and Repo markets. We inactivity from the buy-side, with our borrowers now (September 2024), and related expectations of how this will a sign of muted buy-side activity. We haven‘t observed

have seen significant increases in on-loan balances but rather seeking longer terms and diverse collateral to create impact markets. The evolution in the role of central banks real liquidity pressure, and if any, it‘s been mild and event-

against this a dynamic of significant spread compression. value. The increased demand from borrowers to access is much discussed (increasingly having become lenders of specific, briefly driving up fees or causing supply shortages

Globally the figures reported by the likes of S&P paint a liquidity on term is an interesting dynamic, it represents a “first” rather than “last resort”). Substantial liquidity remains for certain bonds. In April, we observed some specialness

picture of declining revenue and underperformance. We way for beneficial owners to unlock additional value from in the European Fixed Income market, with €3 trillion on two BTPs, related to pressure on liquidity due to a lack

began to observe the onset of spread compression in Q4 their portfolio, whilst allowing borrowers to access liquidity still held at the ECB, down from a peak of €4.8 trillion of activity in the repo market from beneficial owners. This

2022, indicating excess supply in European bond markets, that enables them to meet their regulatory capital ratios in November 2022. The European repo market has seen situation triggered a reaction from the Italian Ministry

resulting in fewer bonds trading at special rates compared (regulatory compliance being a key focus). We think this is a muted demand for government bonds, with minimal specials of Economy and Finance (MEF) to add liquidity via repo

to the general collateral (GC) rate. For example, out of 84 healthy mutually beneficial dynamic. activity. Most European government bonds trade at general operations with the outcome being a swift resolution for

German Bund issuances, 40 were trading at over 20 basis By H1 2024 fast money had moved to the US, and to Japan, collateral (GC) levels. market liquidity.

points (bps) above GC. Today, only 8 issuances exceed 8 which is a market that has seen massive growth as the

bps. This trend was a direct result of the end of the rate Bank of Japan has begun to move to end its yield control

hike cycle, which culminated in the summer of 2023, with curbs. Market participants have been primarily focused on

the Federal Reserve’s last hike occurring on July 26, 2023, financing rather than short coverage, driven by expectations

and the European Central Bank (ECB) concluding its hikes of imminent rate cuts. The ECB reduced rates by 25 basis

on July 27, 2023. Repo spreads have since remained points in June, with the Bank of England following suit

compressed, with European government bonds seeing in August and the Federal Reserve anticipated to follow

subdued borrowing demand.

with at least a 25 basis point cut in September. We note a

Early in the rate hike cycle, the buy-side shorted bonds and decoupling of the monetary policy stance of the ECB versus

bought futures, boosting demand for short coverage. This the Fed and look cautiously at the policy shift from the BOJ

activity in European government bonds created volatility and which could prompt domestic investors to favour local over

opportunities for incremental portfolio yield. However, as foreign bonds, in addition to the role it will play in unwinding

rates plateaued and market anticipation of rate cuts became large carry trades present in the market with the potential

priced in, positioning has now shifted to long. impact of introducing significant additional volatility.