Page 15 - 2808_24_Jan_ISLA_Market_Report_-_Aug_2024

P. 15

14 Securities Lending Market Report | H1 2024 15

Corporate and Emerging Market Bonds Collateral Management Trends

Corporate bonds largely outperformed Treasuries in the first half For securities lending taking the full H1 view Corporate bond The triparty collateral management landscape has seen an As the final Basel III Rules take effect, commercial banks are

of the year, supported by higher income payments and falling markets have shown stable activity levels. Despite stable increase in balances. With the ESTR overnight rate consistently confronted by higher regulatory capital costs. These changes

spreads. However late July and into August market volatility activity, notable fee erosion continues, (reflecting broader trading below the GC repo rate. This trend indicates that will result in banks potentially being required to allocate

caused investors to pare back corporate bond holdings in market conditions) though some specialness persists in certain many financial counterparties lack the optionality to optimise substantially more capital against their trading and financing

favour of government bonds. In the US weaker than expected names. their cash positions without direct access to central banks or activities. How you trade and who you trade with is increasingly

employment and manufacturing data stokes fears of recession adequate repo capacity. The imbalance in collateral supply important. We see our customers wanting to diversify their

and pushes down Treasury yields with a corresponding inverse and demand underscores the importance of efficient collateral counterparty base, to access broad and diverse sources of

move for corporate bond spreads. management strategies. A clear trend has emerged for the liquidity and to diversify credit risk. We see specific demand to

market to increasingly opt for the use of non-cash collateral, swap own covered bonds versus covered bonds of other banks

in parallel with the elevated rate environment and additional to enhance LCR. On the repo side we see increased demand

focus market participants pay to the topic of trading inventory and focus for our clients to access liquidity from corporate,

and collateral optimization. Within “non-cash” we see an sovereign and public sector entities (specifically on term) in

increasing role for both equities and Investment fund shares. In order to benefit from advantageous RWA and NSFR. Worldwide

addition we see increasing demand towards the diversification money market funds (MMFs) saw record net inflows of almost

of collateral (repo) towards the traditionally harder to finance EUR 1.4 trillion over 2023, with about EUR 1 trillion of these

assets in particular CLO’s. In the eurozone this is certainly net inflows in the United States. The result of this is similarly felt

partially attributable to the tapering of TLTRO which results in in securities finance markets.

adjustments to financing markets, with a reduction in Central

Bank pledges offset by growing appetite in interbank markets.

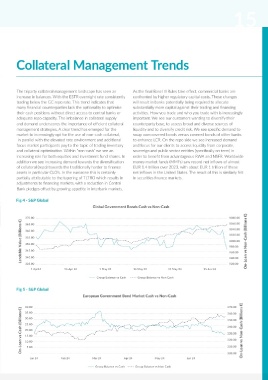

Fig 4 - S&P Global

Introducing the Global Government Bonds Cash vs Non-Cash

ISLA Securities Lending 370.00 1080.00

1060.00

365.00

1040.00

360.00

& Borrowing Hub On-Loan vs Cash (Billions €) 355.00 1020.00 On-Loan vs Non-Cash (Billions €)

1000.00

350.00

980.00

345.00

960.00

Your ultimate resource for all securities lending 340.00 940.00

920.00

335.00

and borrowing information 1 Apr24 16 Apr 24 1 May 24 16 May 24 31 May 24 15 Jun 24

Group Balance vs Cash Group Balance vs Non Cash

Learn about the Key Market Participants Fig 5 - S&P Global

Deep Dive into the Benefits of Securities Lending European Government Bond Market Cash vs Non-Cash

Get your Questions...Answered 40.00 370.00

On-Loan vs Cash (Billions €) 25.00 340.00 On-Loan vs Non-Cash (Billions €)

Access the Latest Market Data 35.00 360.00

30.00

350.00

20.00

330.00

15.00

Scan to find out more 10.00 320.00

310.00

5.00

-

Jan 24 Feb 24 Mar 24 Apr 24 May 24 Jun 24 300.00

Group Balance vs Cash Group Balance vs Non Cash