Page 12 - 2808_24_Jan_ISLA_Market_Report_-_Aug_2024

P. 12

12 13

Securities Lending Market Report | H1 2024

US Treasury Market

>>> US Treasury Market

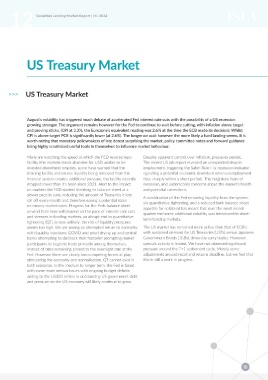

August’s volatility has triggered much debate of accelerated Fed interest rate cuts with the possibility of a US recession Fig 3 S&P Global

growing stronger. The argument remains however for the Fed to continue to wait before cutting, with inflation above target North American Government Bond Market

and proving sticky, (CPI at 3.3%, the Eurozone’s equivalent reading was 2.6% at the time the ECB made its decision). Whilst

CPI is above target PCE is significantly lower (at 2.6%). The longer we wait however the more likely a hard landing seems. It is 2.95 1.00

worth noting that monetary policymakers of late detest surprising the market, policy committee notes and forward guidance 0.98

being highly scrutinized useful tools in themselves to influence market behaviour. 2.90 0.96

0.94

Many are watching the speed at which the FED reverse repo Despite apparent control over inflation, pressures persist. 2.85 0.92

0.90

facility (the markets shock absorber for USD unable to be The recent US job report revealed an unexpected drop in Lendable Value (Trillions $) 2.80 0.88 On-Loan Value (Trillions $)

invested elsewhere) empties, some have warned that the employment, triggering the Sahm Rule— (a recession indicator 2.75 0.86

0.84

draining facility and excess liquidity being removed from the signalling a potential economic downturn when unemployment 2.70 0.82

financial system creates additional pressure, the facility recently rises sharply within a short period). This heightens fears of 0.80

dropped lower than it’s been since 2021. Alert to the impact recession, and underscores concerns about the market’s health 2.65 0.78

on markets the FED started shrinking its balance sheet at a and potential corrections. Jan 24 Feb 24 Mar 24 Apr 24 May 24 Jun 24

slower pace in June, reducing the amount of Treasuries it lets A combination of the Fed removing liquidity from the system, Group Lendable On-Loan Balance

roll off every month and therefore easing a potential strain via quantitative tightening, and a reduced bank balance sheet

on money-market rates. Progress for the Feds balance sheet appetite for collateral has meant that over the most recent

unwind from here will depend on the pace of interest-rate cuts quarter end some additional volatility was introduced in short-

and stresses in funding markets, an abrupt end to quantitative term funding markets.

tightening (QT), is now unlikely, the risk of liquidity pressures

seems too high. We are seeing an attempted return to normality The US market has remained more active than that of EGB’s,

with liquidity injections (COVID and prior) drying up and central with sustained demand for US Treasuries (USTs) versus Japanese

banks attempting to dial back their footprint prompting market Government Bonds (JGBs), driven by carry trades. However,

participants to begin to trade primarily among themselves. specials activity is limited. We have not observed significant

Instead of rates remaining pinned to the overnight rate at the pressure around the T+1 settlement cycle. Merely some

Fed. However there are clearly two competing forces at play, adjustments around recall and returns deadline, but we feel that

stimulating the economy and normalisation, QT cannot exist in this is still a work in progress.

both scenarios. In the medium to longer term, the Fed is faced

with some more serious issues with ongoing budget deficits

adding to the US$35 trillion in outstanding US government debt

and pressure on the US economy will likely continue to grow.