Page 32 - ISLA_SLReport_Feb2021_final

P. 32

Global Equity

Markets in Focus

The second half of 2020 saw global equity markets follow and lenders reacted to the changing sentiments of their Whilst the pattern of data relating to the availability of Earlier in this review we considered the events in

a path of broadly sustained growth, as they recovered from underlying clients. Equity securities being made available equities for securities lending clearly reflects actual market November, when the announcement of the approval

the lows seen in the first half of the year. As further waves for lending rose by some 20% during the half-year, rising events, the pattern of on-loan balances appears more of a COVID-19 vaccine prompted one of the largest

of the pandemic swept across the world however, markets from €14 trillion on 30 June to just under €17 trillion complex. Review of the S&P 500 index highlights how momentum changes ever seen in investment markets,

reacted violently at times. Consequently, although most at the year-end. As discussed earlier in this report markets rebounded strongly from a half-year low point sparking considerable losses within the quant-based

global indices closed 2020 up on the year, it was at times however, key equity indices themselves rose significantly in the final week of June, to rally strongly up until early alternative investment management sector. More broadly,

something of a roller coaster ride. during this period. Consequently, most if not all of September. In contrast during that same period, we saw the final quarter saw wider demand to borrow equities,

this increase was most likely directly related to asset the value of equity securities on-loan broadly fall. particularly in North America where a rush of Initial Public

Inevitably, many of these global themes were played out price appreciation, rather than new assets being made Offerings prompted an increased demand to borrow

in the equity securities lending markets, as borrowers available for lending. The reasons behind this trend are likely to be varied but securities as traders positioned themselves around these

are most likely associated with rising stock markets forcing issues.

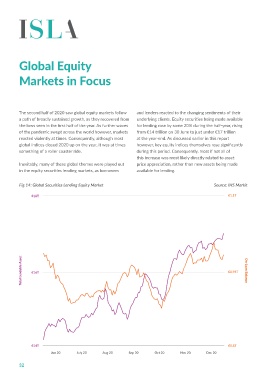

Fig 14: Global Securities Lending Equity Market Source: IHS Markit short sellers to close out positions. As the rest of the year

unfolded, we also saw on-loan balances build again into In Europe we saw less of the trading volatility seen

€18T €1.1T the final quarter, only for the market to then suffer from primarily in North America, with on-loan balances falling

further volatility associated with new outbreaks of the into the year-end to close at €163 billion, compared to

virus and related lockdowns. €195 billion six months earlier.

Fig 15: European Securities Lending Equity Market Source: IHS Markit

€2.7T €220B

Total Lendable Asset €16T €0.95T On-Loan Balance

Total Lendable Asset €2.4T €160B On-Loan Balance

€14T €0.8T €2.1T €100B

Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20 Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20

32 33