Page 34 - ISLA_SLReport_Feb2021_final

P. 34

We saw some specific borrowing around securities

associated with either pandemic-sensitive names in areas

such as the travel industry, or companies that may have

been exposed to the details associated with the final trade

deal between the EU and the UK owing to Brexit. More broadly, the final quarter saw wider demand to

borrow equities, particularly in North America where a

rush of Initial Public Offerings prompted an increased

demand to borrow securities, as traders positioned

themselves around these issues.

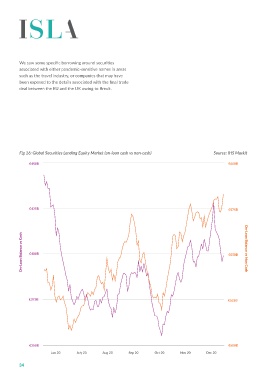

Fig 16: Global Securities Lending Equity Market (on-loan cash vs non-cash) Source: IHS Markit

€450B €600B

From a collateral perspective, the equity market is In closing this review of equity markets and

traditionally one that is split 60/40 between non-cash notwithstanding that the issues around GameStop have all

and cash collateral transactions. The second half of the occurred in early 2021, these are potentially fundamental

year tends to conform to those parameters, but it is shifts in the way markets work that cannot be ignored.

interesting to note that as balances rose, particularly into

€425B €575B the September quarter-end, all incremental business would There has already been considerable debate in the media

appear to have been against non-cash collateral. Again, about the specifics of the GameStop situation that will

the reasons behind this pattern of data may be mixed, but play out over time. What is important here is not perhaps

as borrowers saw the value of their own equity inventory how a poorly performing company in an obsolete market

On-Loan Balance vs Cash €400B €550B On-Loan Balance vs Non Cash collateral. Also, as we have outlined before, lenders may be perspective, but how that has happened outside of the

segment has been transformed from a stock market

positions increase, they were able to use more of them as

normal channels that we are all familiar and comfortable

reluctant to receive cash collateral over key reporting dates,

with. We have seen many times in the past how long-

as short-term investment opportunities are likely to be

only investors have countered short-side participants by

constrained or even destroy value if the reinvestment is in

a currency where short rates are either at zero or negative.

In contrast to the volatility seen in respect of non-cash buying the underlying stock.

What is different here is where that buy-side momentum

collateral, cash collateral remained constant over the has come from, and how the inherent power that

period. Amid limited reinvestment opportunities as technology through the internet has enabled retail

€375B €525B global interest rates have remained at historically low investors to disintermediate the traditional investment

levels, we might have expected a greater drift away from management conduits and engage in markets directly.

the use of cash collateral. However, many funds notably This is worrying for regulators, who instead of being

in the US are not able to accept non-cash collateral at faced with heavily regulated entities at each point in the

this time. Consequently, the circa 40% of all collateral value chain, are suddenly faced with almost a populist

that is in the form of cash should be seen as something movement. This is very new territory for everyone

of a regulatory-driven resistance point, rather than involved, and now that the genie is out of that particular

€350B €500B necessarily the most efficient form of collateral that bottle, it is unlikely to be the last time we will be talking

Jun 20 July 20 Aug 20 Sep 20 Oct 20 Nov 20 Dec 20 borrowers could offer to lenders. about direct action of retail investors.

34 35