Page 31 - ISLA_SLReport_Sep2019

P. 31

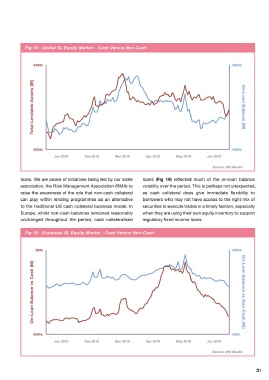

Fig 16 - Global SL Equity Market Fig 18 - Global SL Equity Market - Cash Versus Non-Cash

€14,000k €1,100k €480k €650k

Total Lendable Assets (M) On-Loan Balance (M) Total Lendable Assets (M) On-Loan Balance (M)

€10,500k €825k €350k €500k

Jan 2019 Feb 2019 Mar 2019 Apr 2019 May 2019 Jun 2019 Jan 2019 Feb 2019 Mar 2019 Apr 2019 May 2019 Jun 2019

Source: IHS Markit Source: IHS Markit

increase in on-loan balances through May into early June, the preponderance of non-cash collateral to increase over loans. We are aware of initiatives being led by our sister loans (Fig 19) reflected much of the on-loan balance

indicating some seasonality across the market. time, it has been stuck at around 60% globally for some association, the Risk Management Association (RMA) to volatility over the period. This is perhaps not unexpected,

time now. This relationship did not change significantly raise the awareness of the role that non-cash collateral as cash collateral does give immediate flexibility to

The role played by non-cash collateral, particularly in during the first six months of the year (Fig 18) can play within lending programmes as an alternative borrowers who may not have access to the right mix of

fixed income markets is now well understood. In equity to the traditional US cash collateral business model. In securities to execute trades in a timely fashion, especially

markets, we have seen a constant drift towards the use In North America, non-cash collateral remains around Europe, whilst non-cash balances remained reasonably when they are using their own equity inventory to support

of non-cash collateral as well. Although we would expect 46% to 47% of all collateral pledged in respect of equity unchanged throughout the period, cash collateralised regulatory fixed income loans.

Fig 17 - European SL Equity Market Fig 19 - European SL Equity Market - Cash Versus Non-Cash

€2,300k €280k €80k €200k

Total Lendable Assets (M) On-Loan Balance (M) On-Loan Balance vs Cash (M) On-Loan Balance vs Non-Cash (M)

€1,900k €0k €20kk €50k

Jan 2019 Feb 2019 Mar 2019 Apr 2019 May 2019 Jun 2019 Jan 2019 Feb 2019 Mar 2019 Apr 2019 May 2019 Jun 2019

Source: IHS Markit Source: IHS Markit

30 31